Remember me

Knowledge is “non-rival” (able to be used by everyone simultaneously) and so open access to the results of science confers positive externalities (any firm can develop innovations based on those findings, promoting advancement of science and technology generally, possibly in unexpected ways) and spillovers (strengthening the industrial base, human capital, etc.) [17, 18]. However, if a firm tries to make these results exclusive (blocking or monetising publication), then the externality value is lost. On the other hand, if the knowledge is non-exclusive (freely accessible to everyone), there is a “free rider” problem, meaning there are few incentives to conduct the research if the entity cannot benefit from the rewards.

3.1.1 Basic ScienceBasic research in the life sciences discovers the processes that underlie living organisms and provides the scientific basis for subsequent phases [19]. In pharmaceutical fields, in general only a few compounds progress to the preclinical stage (often lasting 2–3 years) during which the best molecules are selected using various experiments (hit to lead, optimisation, pharmacokinetic studies, toxicity testing, efficacy testing) [20]. In parallel, the firm will develop manufacturing at scale and quality control. Once a candidate molecule is selected, the first clinical studies can start in humans to assess safety, dosing, efficacy and relative efficacy, with the aim of generating the evidence base to present to regulatory bodies (focusing on quality, safety and efficacy) and HTA bodies (focusing on additional clinical benefit and other non-clinical domains to support price and reimbursement decisions).

The classic argument for public-sector support in the basic life sciences focuses on Stiglitz’s insight of the potential for knowledge to generate positive externalities and spillover benefits, for example, to spur unexpected new lines of enquiry, or to reduce financial and scientific risk for other actors to undertake further work [17, 21]. However, the value of basic science is unpredictable and may not become apparent for some time. Many scientific discoveries are by chance, but R&D successes do not occur purely at random. Scientists can only learn from the work of others if they have access to this material. Open access promotes validation, reproducibility, transferability, and good governance. Publication of both positive and negative results allows others to build on success and rule out unpromising lines of inquiry [22]. The public sector can also support science by allowing or encouraging open access to anonymised healthcare data for secondary (research) purposes [23, 24]. Furthermore, spillovers arise when R&D benefits other sectors of the economy, such as enhancing productivity or strengthening the education sector. The R&D spillovers are thought to be enhanced by interdisciplinary network and cluster effects [19, 25].

Private actors often have weak incentives to conduct basic science. Patent intellectual property (IP) is not generally granted for discoveries of laws of nature or molecules found “raw” in nature [26]. Even where the IP from a basic science project can be registered, there is a low probability that this investment would eventually result in a tangible commercial product, let alone a positive return for the investor. Basic science is most likely to generate positive externalities and spillovers when the knowledge is a non-exclusive and non-rival public good [18]. Hence, the classic model is for governments to fund basic science, with no conditions (such as fair price clauses, royalties and so on) placed on the use of the knowledge it generates. Such conditions or monetary barriers could end up blocking dissemination of that knowledge, or disincentivising other researchers from using those results and hence stifling the realisation of these benefits. Notwithstanding, there are some open science models of R&D with extensive private sector participation such as campus models and consortium models that promote sharing of results among subscribers while protecting against free-riders [19, 27].

3.1.2 Development of Science, Technology, Engineering and Mathematics ApplicationsAdvances in AI, image recognition, genome sequencing, gene editing, materials science and other science, technology, engineering and mathematics (STEM) areas are generating technologies that are not in themselves a specific medical therapy but are increasingly instrumental in life sciences [19]. Given the large expected spillover on medical R&D, the impact of such instrumental technologies would be maximised if they were made open source, affordably priced and non-exclusive [28]. The challenge for the public interest is to reconcile these two apparently conflicting objectives: to ensure appropriate investment in developing new technology of this kind, and at the same time ensure that the technology is affordable and widely available to stimulate other researchers to use it to develop new healthcare therapies (see case study: CRISPR).

3.1.3 Case Study: CRISPRCRISPR (a gene editing tool) has been finding applications in development of cell and gene therapies and diagnostic tools, as well as other fields such as agriculture and bioenergy. CRISPR was developed in 2012 by researchers at Massachusetts Institute of Technology (MIT) and was spun off with private investor funding. The CRISPR example highlights that bodies that supposedly have an overarching non-profit educational and public-knowledge mission (such as universities) also may have commercial motivations that can undermine the public-interest mission, especially if they need to find additional sources of income. The MIT university sold exclusives to develop CRISPR therapies to the start-up founded by their own researchers. This exclusivity, along with ferocious patent disputes and an unclear licensing situation, has made access to this technology difficult for small and medium enterprises [29].

Spin-offs from academia need external (usually private) investment to grow and continue R&D (Table 2). These investors expect a return that corresponds to the risk they take, with the academic partner providing the underlying science and ensuring that the collaboration retains some strategic public-interest mission, and the private sector providing growth capital, translational science, experience of regulatory issues or commercial acumen.

It would seem then that technologies such as CRISPR require a particular technology transfer model to realise their potential for spillover benefits. The case for public-private partnerships or social enterprise that combine the best attributes of public and private enterprise is particularly strong in these areas (the “collaborative approach” described in Table 2). This kind of conditionality or reciprocity suggests an “entrepreneurial” public-sector R&D policy/strategy, along the lines proposed by Mazzucato [30].

3.1.4 Development of “Publicly Owned” TherapiesSome public hospitals, in specialist fields such as advanced therapy medicinal products (ATMPs), are acting as a developers. Hospitals in the EU can develop custom-made therapies for named patients where no other option is available under special “hospital exemption” regulations. Some hospitals are taking this a step further and seeking centralised marketing authorisation, for example, ARI-0001, a gene therapy developed in a Spanish public hospital [31, 32]. The stated justification for the public sector taking a leading role or co-owner as a potential marketing authorisation holder for ATMPs is two-fold: to provide a therapy for populations where there are no or few other options [33], and at a price lower to the NHS than a for-profit developer would charge [32]. Nevertheless, there are counter-arguments. The argument that the publicly owned therapy will be provided “at cost” begs the question of how this cost has been calculated. For example, the methodology published by the Spanish Ministry of Health supposes that cost comprises the direct marginal cost of manufacturing the medicine, plus a percentage mark-up of between 1% and 5% for “incentives” [34]. It does not mention the R&D cost incurred, nor a compensation for the risk of R&D failures (sunk costs), nor a compensation for the cost of capital. Each of these elements contribute to the opportunity cost, and would be required in the price of a private-sector commercial product. A price of a therapy that does not include those elements assumes that capital is free, and only acknowledges the upside benefits of successful R&D but not the downside risks of failures (see Sect. 3.2, on the motivations of actors, and Sect. 3.4, on the cost and returns to R&D). A developer that commercialises a medicine at a price that excludes elements of full economic cost could be undercutting fair competition [35]. The government is also regulator of the market, and as such, has a duty to enforce a level playing field. There is a concern that the imperatives of the public-sector payer to pay low prices, working together with a public-sector developer keen to invest in new therapies, could conflict with the market regulatory role of the public sector (see Sect. 3.5, on the role of the public sector as a regulator) (Table 1).

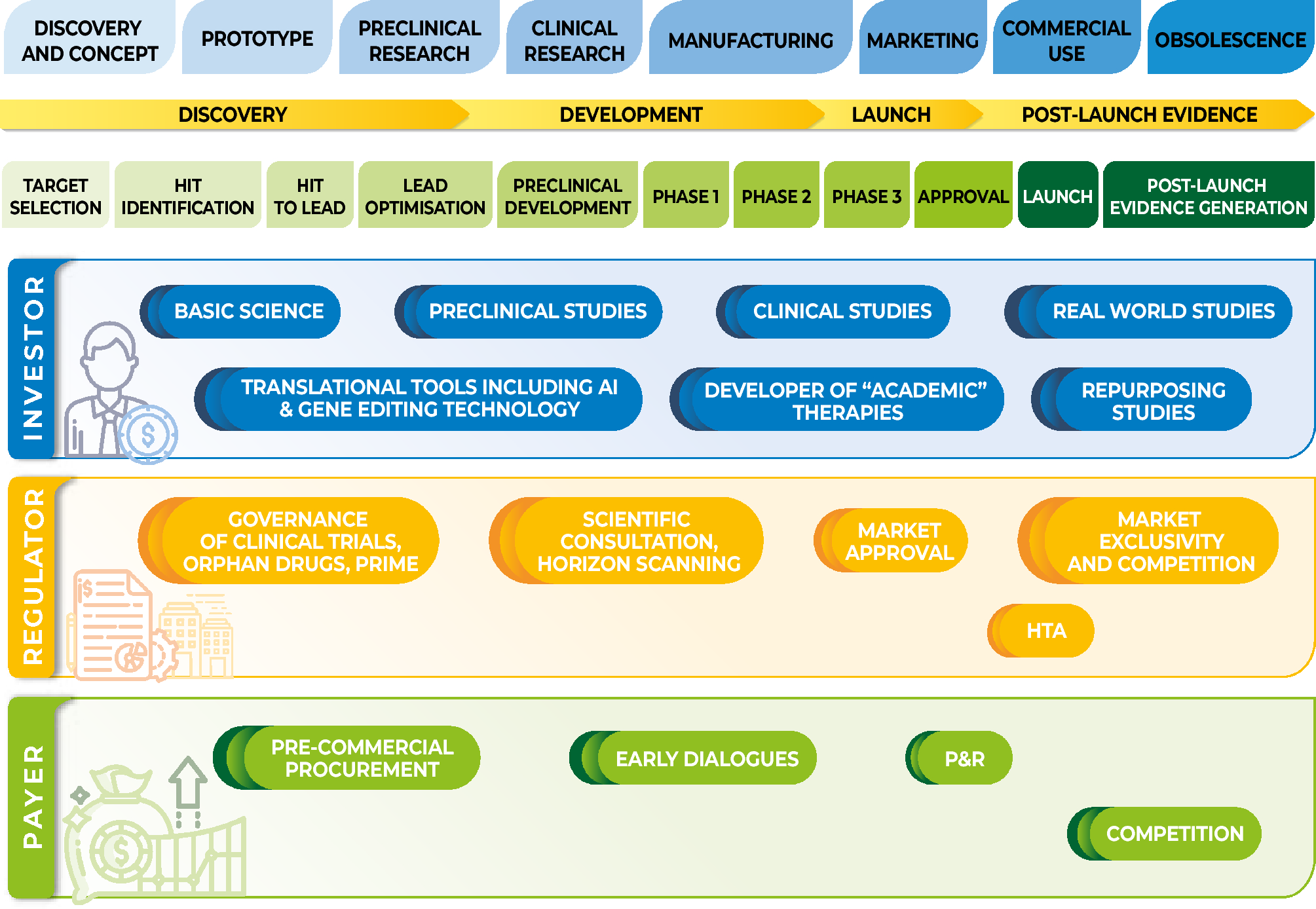

Table 1 Seven possible archetypes of potential development routes to launch3.1.5 Translational StudiesIncentives for private sector investors are weakest in the “translation gap” from basic science to preclinical phases [10] (Fig. 3). For non-orphan medicines, risk-adjusted eNPV is negative at these stages [10]. Hence, private sector investment in these very early stages, if undertaken at all, tends to be financed by investors with a high appetite for risk, variously termed seed capital investors, angel investors, venture capital and so on. Within “translational” technological transfer models (Table 1), risk-seeking early investors often aim to take a discovery to the preclinical stage and sell the IP to mainstream corporations (merger and acquisition, M&A).

The private venture capital industry is a very specialised sector, and there are likely to be many promising emerging technologies that do not get this kind of support. Moreover, venture capitalists will expect a high and rapid rate of return to compensate the high risk, which, alongside the substantial legal fees and commissions involved in M&A, filter through into higher prices. Hence there may be here an economic justification for public-sector or non-profit support for promising technologies to help bridge this “translational gap”.

Although research at this stage has a low probability of commercial success (Table 2), it is conceptually and qualitatively distinct from basic science. Translational research is applied science, meaning that it is oriented towards producing a specific therapeutic product that has a readily available or creatable market. In the case that these data have a potential commercial value, companies have an incentive to invest, although they will be aiming to keep the IP exclusive. This suggests that the public sector should only consider investing scarce research capital in translational research (and later applied stages) if there is a clear public interest that cannot be met by the market.

Table 2 Risk of failure, out-of-pocket costs and capitalised costs along the life cycle3.1.6 Real-World Studies and Repurposing StudiesEven after a product obtains market approval, further studies on the use of the therapy in the real-world setting may have value to practitioners and health systems (in addition to the usual pharmacovigilance). Doctors may be able to optimise the duration or dose of therapy, identify the most effective subgroups, or mitigate environmental damage from residues. However, the marketing authorisation holder has weak economic incentives to voluntarily conduct post-marketing studies that would lead to lower revenues (for example, that might occur if a study showed a lower dose is as safe and effective as a higher dose and price depends positively on strength). Repositioning or repurposing is the use of existing medicines in new indications after expiry of intellectual property rights (IPR) [36]. Likewise, there can be few incentives for either the originator brand or generic manufacturers to conduct the necessary clinical studies to obtain market approval for the potential new indication after loss of market exclusivity. There may be an a priori justification for public-sector or non-profit investment to conduct real-world and repurposing studies, whose results may lead to cost savings and/or benefits to patients.

3.2 The Motivation of Public-Sector ActorsThe public sector, even within a single country, is not monolithic but acts through multiple entities with different objectives, degrees of independence and sources of finance (Fig. 1). Public Choice theory suggests that the actions of all actors, public and private, are shaped by the institutional context and incentives, and its institutions can be captured by special interests [37, 38]. The State is unlike other bodies, in that it requires citizens to be members, and imposes obligations (such as paying taxes and/or obeying regulations) on private individuals and businesses. Hence, checks and balances are essential to ensure that government actions do not favour public-sector or private-sector special interests without good reason [39].

Public investment in R&D is likely to have the greatest potential societal impact when it addresses a clear market failure or can springboard private-sector investment [40]. The ex ante justification for public-sector engagement might be weaker where the aim of the R&D is to commercialise a specific therapy (for example, phase 2 or 3 studies, Fig. 1). Recognition should be made of the possible trade-offs or unintended consequences of this action. Public-sector applied research may compete with the private sector, and State Aid should not result in unfair competition, or crowd-out private sector incentives. Because the State has the power to meet debt obligations by increasing taxation, the cost of borrowing for the public sector is usually lower than for commercial companies, but this does not mean the public sector is better placed to take on high risk R&D [14, 41]. The cost of capital should recognise that public funds invested in R&D might displace expenditure in other public services or require higher taxes.

Hence, an important element of governance in public R&D is to carefully justify, ex ante, the expected societal benefits and opportunity costs, and take steps to mitigate the risks and unintended consequences. If the public sector chooses to engage in applied R&D, this activity should be justified, financially sustainable and transparent. Research and development is inherently risky, and failures are inevitable and costly. This suggests public applied R&D should not be ad hoc (“individual project by project”), but conducted as part of coherent strategy. These considerations may justify public-private collaboration [42, 43]. The partner might offer commercial management expertise such as setting achievable objectives, capital and tools to measure and manage the risks. The entity should enjoy the legal autonomy to own IPR, use the IPR to generate revenues, to retain and reinvest financial surpluses, be able to reward success and learn from failures, and be subject to accounting rules that require prices fully reflect all the opportunity costs, including the costs of capital and the costs of R&D failures.

Nevertheless, the entity or collaboration should have a public interest mission, rather than profit-maximising. In the case of a STEM technology such as gene editing tools, it seems in the societal interest that such a collaboration sells non-exclusive rights to use the technology to any interested third party at an affordable price. This would allow access to this technology by small and medium-sized enterprises, who are the type of actors who would be most adept at seeking out multiple ways of exploiting it to produce innovations that could benefit patients. An unconditional spin-off or acquisition of the technology by a large corporation is more likely to result in exclusivity, limiting the potential benefits. The CRISPR example (Sect. 3.1.3) illustrates that it cannot be assumed that academic and public research groups automatically adhere to a public-interest mission. It is not clear how such institutions could be persuaded, incentivised or obliged to take a “benevolent” societal perspective [38]. There is a case for reconsidering how academic spin-offs should be governed and capitalised. Crowd funding or social bonds may offer potential mechanisms (Fig. 2).

Fig. 2

Objectives of R&D activity and policies. Source: Produced by authors, based on their interpretation of the literature. a. Examples of spillovers: sustainable R&D environment, employment, productivity; b. Examples of externalities: diffusion of knowledge, advancement of science. HTA Health Technology Assessment, R&D research and development

3.3 Models for Regulation of PricesFor new medicines and health technologies, payers often use HTA to evaluate the evidence and guide P&R decisions. Essentially, payers are aiming to establish whether the technology offers positive “net benefit” or value for the health service, and so should be adopted at the price offered by the manufacturer [44]. However, there is no clear consensus about how this value should be defined, measured [45], and ultimately shared between the payer and the developer [46]. The concept of the “value-based price, VBP” represents the maximum price that the payer would be willing to pay for the technology, and this should set the upper limit for decision making about actual prices and reimbursement policy.

A few countries formally express net benefit as a formula (Eq. 1). For example, in the UK health is measured in terms of the quality adjusted life year (QALY), and costs in terms of the resources used by the national health service; λ represents the opportunity cost of health that might be displaced by adopting a new intervention (or “threshold”). For countries using this methodology, the value-based price represents the (theoretical) price that will make the net benefit exactly equal to zero:

$$} = } \times \lambda }$$

(1)

It has been frequently suggested that the value-based price provides a (theoretical) equilibrium between the demands of the payer (higher prices displace health care and health from other patient groups) and the objectives of developers and investors (higher prices encourage future investment in those therapeutic areas) [7, 15, 47]. If a health service payer wishes to encourage development of new therapies in certain areas (such as unmet need, rare diseases, etc.) this can be signalled in the framework of Eq. 1 by declaring a higher value of λ for these areas than other cases [48, 49].

Value-based price is a normative concept, not a description of a particular methodology. It recommends that health services should estimate its maximum willingness to pay for a given therapy according to the “therapeutic utility” it provides to patients, and perhaps other beneficiaries (such as carers) or even beyond health care if a societal perspective is adopted.

Few countries calculate incremental net benefit by cost-effectiveness analysis (CEA) with a published value for λ. Countries such as Sweden conduct CEA but do not publish λ. Nevertheless, a signal can be tacitly observed through the approval/rejection decisions of the P&R process. France and Germany de facto apply a VBP concept by estimating comparative clinical effectiveness using a rigorous methodology, which then determines the boundaries for price negotiation.

Value-based price has two important corollaries for R&D. First, if a developer wishes to charge more than the value-based price, the payer should reject that application and precisely indicate the reasons. The negative decision provides a meaningful signal to future developers about the priorities in that country’s health service. Second, value-based prices are not determined by the cost incurred by the developer. That is, health services must not be lured into paying high prices “because new therapies are costly to develop” [50]. This reverse-thinking would imply a form of “cost-plus” pricing. Cost-plus pricing can be distorted by information asymmetry between developer and payer. Moreover, the method does not provide efficient dynamic signals to guide future R&D as it creates incentives for the industry to pursue innovations with high development or manufacturing costs rather than focusing on providing high health benefits. Likewise, external reference pricing disassociates the price of a therapy from its therapeutic impact [51]. For example, Singh notes a tendency for developers to pursue biologic therapies based on their high expected reimbursement price, rather than consider small molecule therapies that might have a similar incremental therapeutic benefit but see payers usually reimbursed at lower prices [19]. Value-based pricing sends a signal that the industry must only bring therapies with costly R&D to market where it can demonstrate commensurately large therapeutic benefits.

Nevertheless, there are several ways that value-based pricing signals only imperfectly convey payers’ interests and priorities. One reason is information asymmetry between the developer and the payer. The developer chooses which molecules to investigate; the timing of clinical studies; and proposes the key parameters of the estimand [52] (in HTA usually referred to as PICO: population, intervention, comparators, outcomes). Second, there are many payers (given medicines are usually developed to serve multiple countries and regions), and any individual payer’s influence on R&D through its pricing decisions depends on the value of the market. Because of the long timelines from laboratory to market, developers will be most responsive to coordinated, durable and predictable price signals [46]. Third, healthcare regulators also set policies and provide incentives that impact on revenues and costs of developers, such as accelerated access for unmet need or orphan medicine status (including the Orphan Drug Act and the Orphan Drug Legislation) [53]. While these measures have stimulated investment in orphan medicines [54], they can also provide opportunities for gaming. Developers of a new therapy could exploit loopholes in these regulatory incentives to engage in market differentiation to extract the maximum consumer surplus, for example, positioning the first indication for the therapy as an orphan medicine, and once established in the market with a high launch price, gradually engage in other clinical studies to open up further indications. Some authors have expressed concern that there are now “too many” incentives for orphan medicines in Europe [10].

A criticism sometimes levied at the VBP concept is that developers will set prices up to the VBP, and so the developer will accrue all the value, and the health service will get none. This criticism does not consider that prices tend to fall over time, because of entry of other therapeutic alternatives during the IP protection period, and generic or biosimilar competition afterwards [55]. Hence, it is possible for prices of new branded medicines to be set at the VBP at launch, and for both parties to share the value over the lifetime of the therapy [46]. If, as is quite common, prices are set above the VBP, the value for the health service can be negative [46]. Furthermore, these high prices attract more investment in those areas and therefore will be dynamically inefficient.

Another misunderstanding about monopoly profits from innovations is that they provide the funds for future R&D by the same company. Industrial sectors with higher concentrations are usually not more R&D intensive [56]. Monopoly power can make firms defensive rather than efficient, and the firm may choose to return profits to shareholders rather than invest [14]. Large, liquid capital markets should be able to allocate funds to projects with greatest risk-adjusted expected returns. Traditionally in the pharmaceutical sector, large, diverse firms have been better placed to absorb the high sink costs per individual R&D project and take advantage of economies of scale [56], but recently other models have been successful, particularly in small populations and ATMP [57].

3.4 Models to Measure Costs and Returns to R&DProfit-seeking manufacturers and investors measure the value of the technology in terms of the financial return it can generate, or expected net present value (eNPV, Eq. 2). Other factors may also influence the firm’s decisions, such as building a diversified or synergistic portfolio or being first-in-class:

$$\text= _^_^(p}__-_)/(1+r^.$$

(2)

In Eq. 2, pmt is the price in country ‘m’ at time ‘t’, qmt is the absolute market size for the product in country ‘m’ at time ‘t’, ct is the risk-adjusted R&D and manufacturing cost at time ‘t’, and ‘r’ is the cost of capital of the firm. The time horizon ‘T’ will include time both with and without market exclusivity, highlighting that the market dynamics before and after generics/biosimilar entry can be very different [46]. The developer’s expectations about cost (Table 2) and revenues will enable an estimate of future eNPV at any given stage on the life cycle (Fig. 3), and thereby guide the company’s strategic investment decisions (Table 2).

Fig. 3

Estimated risk adjusted expected net present value for non-orphan and orphan medicines, at each phase of research. Source: Kalindjian et al. [10]. eNPV expected net present value. Illustrative conversion rate: $1 = 0.866 euros (xt.com 14/5/2025)

Table 2 shows how a private firm might calculate the fully capitalised economic cost of R&D per approved product. These estimates are shown for illustration of the underlying concepts, as the numbers vary across sources [1, 10], depending on the data and sample of medicines included. The private firm must take account not only of “out-of-pocket” expenses of R&D (i.e., the direct cash outlay incurred for that product) but two further “non-cash” elements that can be difficult to estimate: (a) the sunk costs of abandoned or failed R&D projects and (b) the cost of capital [7, 58]. The sunk costs already incurred up to time t should not be considered in a stop-go decision about an ongoing R&D project. However, sunk costs from abandoned or failed projects can only be recover

Comments (0)